How Quantitative Tightening Impacts the Stock Market

Quantitative Tightening and the Federal Reserve Balance Sheet

The unwinding of the Federal Reserve’s pandemic-era balance sheet represents a critical inflection point for equity markets, altering the risk-reward calculus for US investors. To understand the magnitude of this regime shift, one must look at the scale of the central bank’s interventions during the COVID-19 economic freeze.

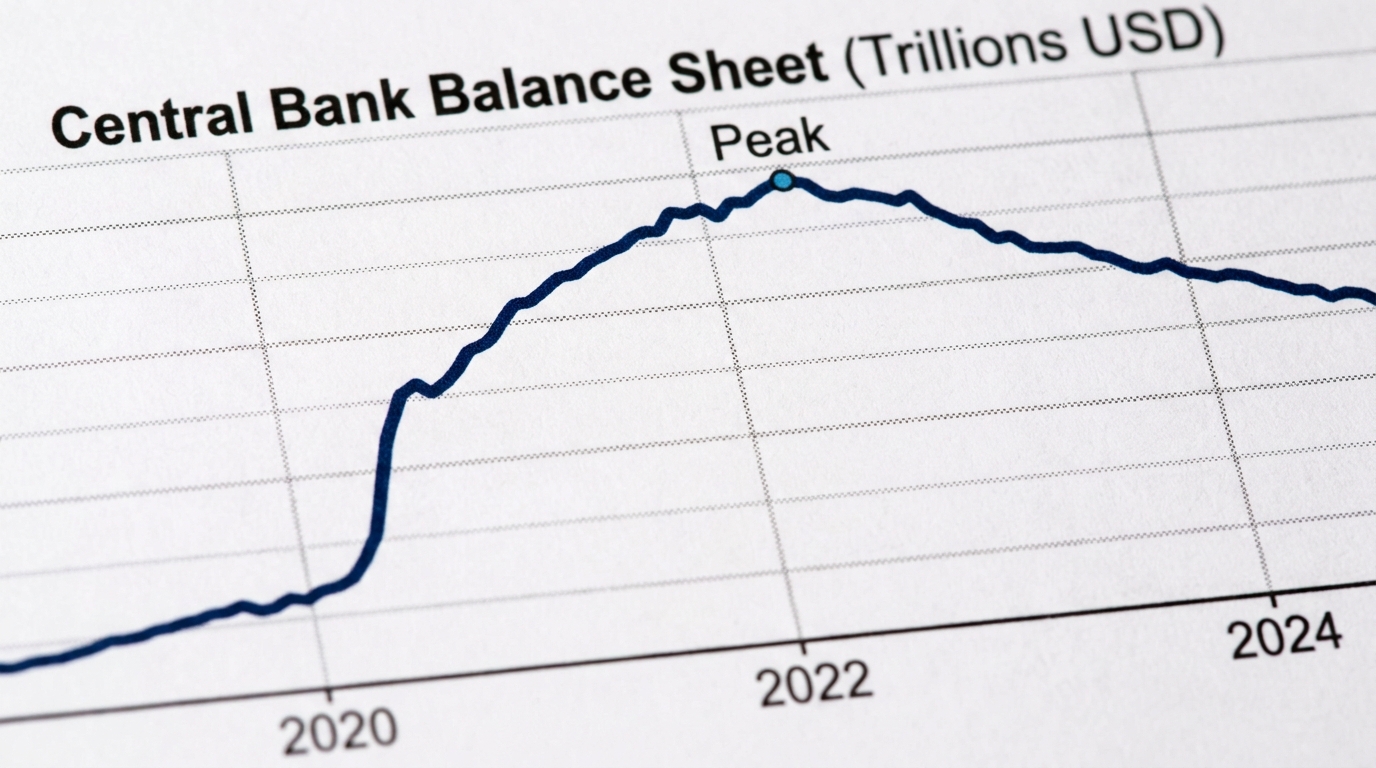

In March 2020, the Fed’s balance sheet stood at $4.3 trillion before entering a period of rapid expansion. By May 2022, these holdings had more than doubled to a peak of $8.9 trillion, at which point the central bank announced it would begin shrinking its securities holdings, according to Brookings.

The transition from this liquidity injection to Quantitative Tightening marks a structural shift in market mechanics. For investors, the withdrawal of this price-insensitive buyer signals an end to the era of abundant capital. Market actions and central bank communications underscore a reality: equities are transitioning into an environment of increasing capital scarcity, where valuation adjustments are driven by shifting discount rates rather than deteriorating economic fundamentals.

The Transmission Chain: From Policy Signal to Asset Repricing

Understanding how balance sheet runoff digests through the financial system requires mapping the specific transmission chain from policy event to market effect. When the Federal Reserve engages in quantitative tightening, it essentially removes excess liquidity from the financial system. During the expansion phase, asset prices were supported by increased liquidity. As that liquidity is withdrawn, the mechanics of the market operate in reverse.

The primary mechanism begins in the fixed-income markets. The liquidity withdrawal directly removes a massive buyer from the Treasury and mortgage markets. Consequently, the absence of Fed demand exerts downward pressure on bond prices, forcing long-term bond yields higher to attract private capital, as noted by Brookings. This upward pressure on bond yields serves as the critical first link in the transmission chain that ultimately compresses equity valuations.

As risk-free Treasury yields climb, the discount rate applied to future corporate earnings rises in tandem. This fundamentally alters how investors price risk and calculate the present value of future cash flows. The mathematical reality of higher discount rates heavily affects long-duration growth and technology stocks.

Because high-growth tech companies derive the bulk of their intrinsic value from cash flows expected many yearsor even decadesin the future, their stock prices are highly sensitive to the compounding effect of higher interest rates. When the risk-free rate rises, the present value of those distant earnings declines significantly. This leads to multiple compression, resulting in sell-offs in the technology sector even if the underlying company’s business model, market share, and revenue growth remain intact.

For market participants, this indicates that quantitative tightening acts primarily as a valuation recalibration tool that directly targets the equity risk premium. As the Fed withdraws its footprint from the bond market, rising Treasury yields naturally compress the premium investors demand for holding riskier equities, forcing a downward revaluation of stock prices across the board.

Decoding Federal Reserve Communications

The market’s sensitivity to quantitative tightening is often less about the actual, day-to-day mechanical runoff of assets and more about the signaling effect of central bank communications. To quantify this market sensitivity, researchers Sydney Ludvigson, Francesco Bianchi, and Sai Ma analyzed 14 specific Federal Reserve communication events regarding balance sheet tapering or tightening between May 2013 and March 2019, according to Brookings.

Their findings isolate the immediate impact of unexpected policy signals on equity valuations, providing clear evidence for how markets digest balance sheet news. According to the research from Brookings, surprises in Fed communications regarding the balance sheet caused the S&P 500 index to move by as much as 2 percent.

This magnitude of single-day movement underscores that equity markets are highly reactive to the perceived trajectory of the Fed’s balance sheet. These equity swings are primarily driven by investors rapidly recalibrating their expectations for equity returns relative to the newly elevated yields on risk-free Treasury securities.

Crucially, the data reveals a disconnect between financial market reactions and underlying real-world economic expectations. The structural model applied to these 14 events revealed a divergence between financial market volatility and real-world economic projections.

| Data Category | Observation | Source |

|---|---|---|

| Verified Fact | Surprises in Fed communications regarding balance sheet tapering cause immediate S&P 500 movements of up to 2 percent. | Brookings |

| Inference | These communication events do not meaningfully alter broader macroeconomic expectations for inflation or GDP growth. | Brookings |

Analyzing this divergence offers an implication for US market participants: balance sheet runoff communications act predominantly as a financial conditions shock, not a macroeconomic bellwether. Structural models applied to these events indicate that surprises in tightening signals do not meaningfully alter market expectations for gross domestic product (GDP) growth or inflation, per Brookings.

If GDP and inflation expectations remain static while equities drop 2 percent, the market is experiencing a mechanical repricing of liquidity and discount rates. This implies that equity drawdowns triggered by quantitative tightening announcements may not signal an impending recession, but rather a temporary liquidity adjustment.

The tech sector’s vulnerability to quantitative tightening is a financial phenomenon driven by the mathematics of discounting. Consequently, investors should be cautious about interpreting QT-induced stock market volatility as a definitive leading indicator for broader economic deterioration. Financial markets can experience turbulence while the broader economy remains relatively unaffected by the specific mechanics of balance sheet reduction.

Scenario Analysis: Navigating the Balance Sheet Runoff

As the Federal Reserve continues to shrink its balance sheet, market participants must navigate a range of potential outcomes. Historical data leaves investors with lingering uncertainties regarding the optimal size of the central bank’s footprint, making scenario planning essential for portfolio management.

The Base Case: Methodical Reduction and Value Outperformance In the base case scenario, the Fed continues a methodical, well-telegraphed reduction of its securities holdings. Under this scenario, the primary implication for US investors is a sustained elevation in the cost of capital. Because balance sheet reductions shifts the relative attractiveness of risk-free assets without inherently damaging aggregate growth expectations, investors demand higher equity risk premiums.

The second-order effect of this dynamic favors cash-rich, defensive sectors and value equities. These mature companies generate robust current free cash flow, insulating them from the need to issue new debt or equity in a liquidity-constrained environment. Businesses with strong balance sheets are insulated from the higher refinancing costs that accompany elevated bond yields. Consequently, value equities emerge as structural winners, as their near-term cash flows suffer less of a discount rate penalty compared to long-duration assets. Navigating this regime requires investors to prioritize near-term profitability and dividend yields over distant growth promises.

The Downside Risk: Systemic Stress and Growth Compression The downside risk scenario poses challenges to debt-reliant growth companies and broader financial stability. If the Fed’s balance sheet reduction triggers an unexpected tightening of financial conditions, the cost of rolling over corporate debt will increase. Growth companies typically rely on continuous external financing to fund operations; as the Fed withdraws capital, the discount rate applied to these companies’ distant future earnings rises. An acceleration in quantitative tightening will lower the valuation multiples of unprofitable technology and speculative growth sectors.

A vulnerability in this downside scenario is the potential for systemic repo market stress. Empirical evidence regarding the exact trigger point for liquidity stress remains thin. Market participants do not know the precise terminal size the balance sheet must reach before liquidity constraints disrupt overnight lending markets. Because historical data lacks a definitive threshold for when normalization crosses from benign policy into systemic risk, investors must treat the endgame of balance sheet reduction with uncertainty.

The Upside Scenario: Seamless Absorption and Controlled Cooling In the upside scenario, the broader economy absorbs the liquidity drain seamlessly, or the Fed successfully tapers its reduction before systemic disruptions occur. A critical component of this scenario involves the unwinding of pandemic-era interventions in the housing market. Economist Arvind Krishnamurthy noted that the Fed’s prolonged purchases of mortgage-backed securities during the COVID-19 pandemic likely fueled a housing boom by artificially suppressing mortgage rates, according to Brookings.

As the central bank reverses course, the withdrawal of this demand removes a key pillar of support for mortgage markets. A controlled, gradual unwind of these specific assets could successfully cool real estate valuations without triggering a broader macroeconomic contraction. If the Fed achieves this balance, the open question of whether QT-driven stock market jumps have any actual relevance for the broader economy may be answered favorably. An upside resolution would stabilize the financial sector, allowing US equity markets to refocus on organic corporate earnings growth.

What to Watch Next: Concrete Indicators for Market Participants

Navigating this environment requires a disciplined focus on a specific set of forward-looking indicators. Because the transmission mechanism from balance sheet reduction to the real economy is not entirely clear, investors must monitor concrete triggers that signal liquidity stress.

- Federal Reserve Press Conferences and Communications: Investors must remain attentive to official policy communications. Upcoming Federal Reserve press conferences are critical volatility catalysts. Market participants must monitor for any surprise communications regarding the pace or terminal size of the balance sheet runoff, as historical data proves these surprises can move the S&P 500 by up to 2 percent.

- Long-Term Treasury Yields: Increases in long-term Treasury yields serve as a leading concrete indicator of liquidity stress. When the market perceives a faster-than-expected balance sheet runoff, the resulting upward pressure on Treasury yields mechanically compresses the equity risk premium. Investors should watch the 10-year and 30-year yields closely as a barometer for discount rate adjustments.

- Housing Market Data and Mortgage Spreads: The housing market stands out as a critical sector for monitoring the real-world impact of the Fed’s balance sheet runoff. Investors must account for a prolonged period of elevated mortgage rates, which will act as a structural headwind for homebuilders, real estate investment trusts (REITs), and consumer discretionary sectors tied to home turnover. Watch for shifts in home price resilience and mortgage spread widening as direct barometers of liquidity withdrawal.

- Short-Term Funding Rates: To guard against the downside scenario of systemic funding issues, market participants should monitor short-term funding rates and repo market dynamics closely. Stress will likely materialize in banking operations before cascading into broader equities.

Conclusion

The transition from monetary expansion to Quantitative Tightening represents a shift in global asset pricing. The evidence demonstrates that while the unwinding of the Federal Reserve’s balance sheet acts as a catalyst for equity volatilitycapable of moving major indices by 2 percent on communication surprises alonethis volatility is predominantly a mechanical repricing of liquidity rather than an indicator of macroeconomic decline.

For investors, the analytical synthesis is clear: the era of central bank-subsidized asset prices has concluded. Market participants must adapt by demanding a higher margin of safety in their equity allocations, rotating away from long-duration, speculative growth assets penalized by rising discount rates, and prioritizing cash-rich, defensive enterprises.

Until the Federal Reserve establishes a definitive terminal size for its holdings, navigating Quantitative Tightening requires treating sudden market drawdowns as valuation adjustments rather than definitive economic warning signs, keeping an eye on Treasury yields and housing data as the primary barometers of systemic liquidity.

Disclaimer: This analysis is for informational purposes only and does not constitute investment, financial, real estate, or legal advice. Always consult a licensed financial advisor before making investment decisions.

FAQ

How does quantitative tightening directly affect stock market valuations? Quantitative tightening directly affects stock market valuations by pushing long-term Treasury yields higher as the Federal Reserve withdraws its demand for bonds. These higher risk-free yields increase the discount rate applied to future corporate earnings, which naturally compresses the equity risk premium and forces a downward revaluation of stock prices.

Why are technology and long-duration growth stocks more vulnerable to balance sheet reduction than value stocks? Technology and long-duration growth stocks derive most of their intrinsic value from cash flows expected far in the future. When quantitative tightening drives interest rates and discount rates higher, the present value of those distant earnings declines significantly. Value stocks with robust current free cash flow are less penalized by these rising discount rates.

Will the Federal Reserve’s balance sheet reduction impact broader macroeconomic expectations like GDP or inflation? Historical structural models indicate that surprises in Fed communications regarding balance sheet tightening do not meaningfully alter market expectations for gross domestic product (GDP) growth or inflation. The resulting equity market volatility is primarily a financial phenomenon and liquidity adjustment rather than a signal of fundamental macroeconomic deterioration.

How did the Fed’s balance sheet expansion impact the housing market, and what happens as it shrinks? During the expansion, the Fed’s sustained purchases of mortgage-backed securities suppressed mortgage rates, fueling a housing boom. As the balance sheet shrinks and these securities roll off, this demand is removed, placing upward pressure on mortgage rates and acting as a structural headwind for homebuilders, real estate valuations, and housing-adjacent equities.